Even if you aren’t a space nerd and don’t follow the industry, chances are you’ve heard about the Chinese Tiangong space station, The Emirates Mars Mission, China landing a robotic spacecraft on the Moon, Russia’s and India’s plans to land on the Moon, impressive successes in gathering samples from asteroids, first flight on Mars, Virgin Galactic’s and Blue Origin’s first fully crewed spaceflights, and, of course, the rapid development of an industry-changing and fully reusable SpaceX’s Starship that may be able to take us to Mars one day.

The space race is back.

Only this time, it’s not going to be just two superpowers racing to the Moon.

This time, with the help of private companies, and Starship leading the way, entire new industries are going to be born.

Just like the invention of the elevator had forever transformed architecture and city design in the late 19th century, Starship has the potential to completely transform the space industry and spark a new era of innovation by simply lowering payload costs.

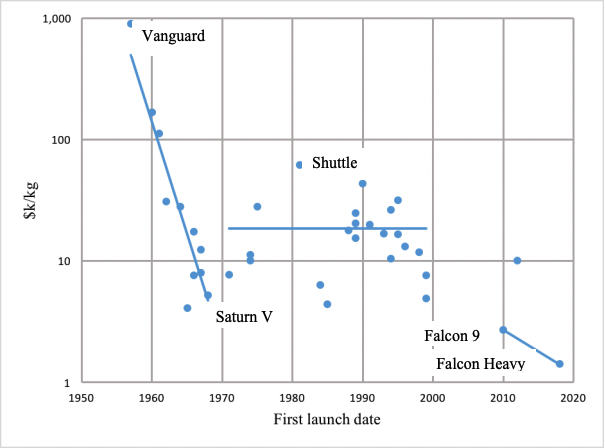

When NASA’s Space Shuttle was in operation, it could launch a payload of 27,500 kg to Low Earth orbit (LEO) for $1.5 billion, or $54,500/kg. Today, SpaceX’s Falcon 9 can offer to send 22,800 kg of cargo for $62M or only $2,720/kg, and Falcon Heavy at $1,410/kg is even more affordable.

Even though this is an astonishing cost reduction by a factor of 20, it’s still inaccessibly expensive for most startups, and that’s one of the main reasons why space has been a realm of governments and companies that mainly rely on government contracts to survive.

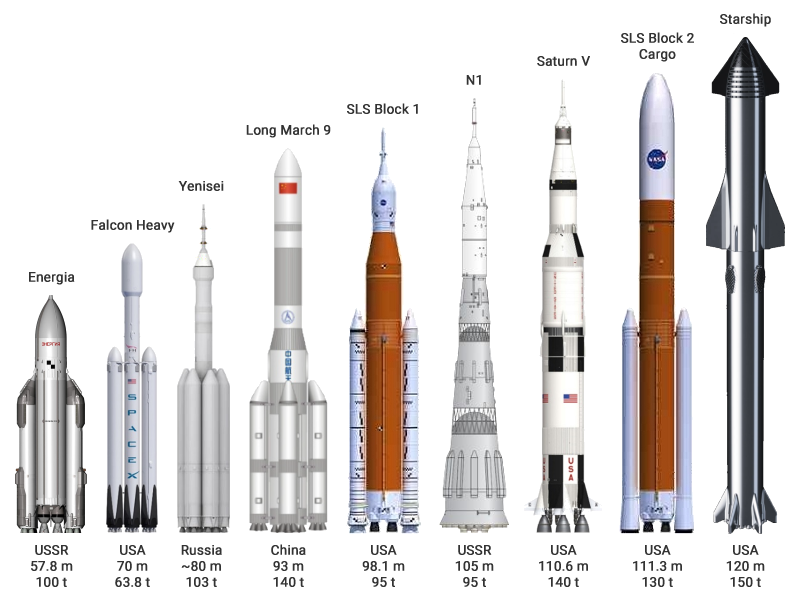

Enter Starship: the tallest (120m), highest-thrust (about double the Saturn V), and only fully reusable orbital rocket in history.

Once complete, it will be capable of lifting 100 metric tonnes to orbit. The booster will run on sub-cooled liquid methane and liquid oxygen propellant and exert 72 meganewtons of force (16,190,000 pounds of force) during liftoff.

If Starship can send 100 tonnes of cargo to orbit, it can also send that cargo from New York to Sydney in less than an hour. For comparison, a Boeing 737 has an empty weight of 45 tons. This can create an entirely new market for space launch, one that involves not a hundred or so launches per year, as is currently the case, but hundreds or even thousands per day, which, in turn, would drive a radical cheapening of space technology.

Elon mentioned that the propellant cost of orbital launch would be about $10/kg, with a marginal cost of Starship mass to orbit under $100/kg, suggesting a roughly $200/kg price tag to LEO, which is an order of magnitude below that of the Falcon 9.

Today, even the most basic 6U CubeSat costs ~$300,000 to make, mainly because it costs about the same to put it in LEO, so you are going to be more than willing to pay premium prices for all your satellite’s components and spare no expense in testing everything to the max.

With the launch costs that low, the cost of all space hardware will radically drop because it will no longer be necessary to engineer all parts to super exacting conditions. Companies will be able to drastically reduce expenses by simply taking on the risk of paying for another launch.

What else will be possible when Starship is fully operational and the launch costs are down by >20X?

Since Starship is designed to be refuelable in orbit, it’ll pave the way for “space gas stations” and significantly increase the market size for companies like OrbitFab.

At the 2016 Recode conference, Jeff Bezos said that building things in space makes much more sense than trying to build them on Earth. Heavy industrial manufacturing should happen in outer space, and the Earth should be zoned for residential living. He wants thousands of entrepreneurs building things in space, but high launch costs remain the main challenge for on-orbit manufacturing.

There are products that could revolutionize life on Earth, but our planet’s constraints—mainly gravity and dust—prevent us from creating them.

For example, gravity makes it virtually impossible to 3D print a heart with its four chambers and highly organized muscle tissue made of different types of cells. On Earth, tissues printed with runny bioinks made of gel and human stem cells collapse under their own weight, and we have to add scaffolds or toxic chemicals, which creates problems in the long run, such as eventual immune reactions to these synthetic scaffolds or inaccurate structures.

This is where microgravity comes to the rescue. Without gravity, cells can freely self-organize into their correct 3D structure without needing a scaffold. Printing in microgravity allows the object to spit out in genuine 3D, improving speed by up to 100 times.

And it’s not just organs.

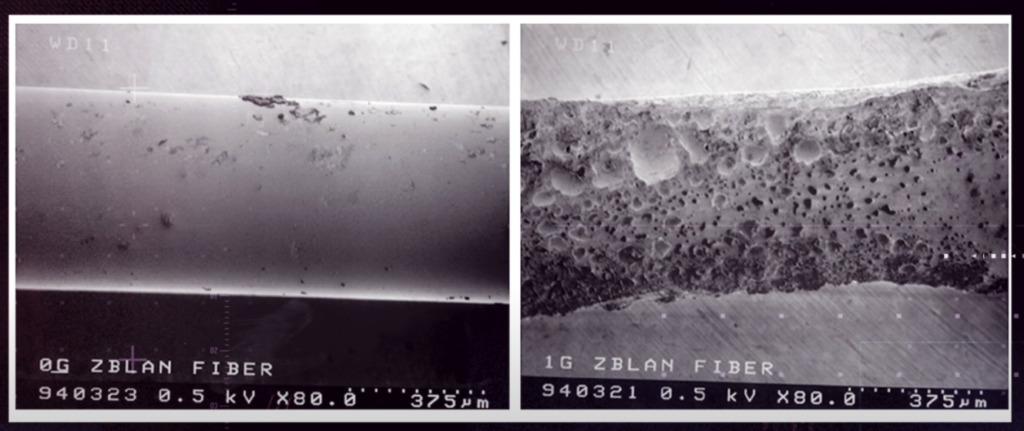

ZBLAN optical fiber made in 0G gravity is 100X more efficient than the silica-based one made on Earth, and gallium-arsenide semiconductor is 10,000 times better in quality.

There are already companies working on making this a reality:

Made In Space has manufactured the first ZBLAN optical fiber on the ISS and working on a robotic assembly machine with an in-built 3D printer; Techshot is working on 3D bioprinting soft tissue, and Varda is planning to be “the Foxconn of Space.”

Carbon nanotubes, metal alloys, and crystallized proteins are just a few more products on the shortlist for space manufacturing today; even with the current launch prices, these products are expensive enough to be profitable. So imagine how many and what kind of new possibilities will be created with >20X better margins.

The year is 2030.

The biggest manufacturing hub isn't in China anymore; it's in space.

Microgravity, ∞ physical space, free solar energy & resources allow us to make carbon nanotubes, ZBLAN, better semiconductors, and 3D printed hearts.

Earth is for residential living only.

— Max Grev (@max_grev) December 17, 2020

Think of how it could allow other companies in the space economy to bypass launch to LEO, fundamentally changing the capabilities of the assets in space. Products like large antennae and giant solar panels that would not otherwise fit in a rocket capsule could be assembled in orbit and joined to more sophisticated parts built on Earth. On-orbit gas stations could fuel newly assembled rockets, which could be built with negligible concern for weight and propellant. And the entire high pollution industries could be relocated to orbit to avoid harmful effects on the environment on Earth.

Given its potential, I believe that on-orbit manufacturing can be the biggest new space market, made possible, in large part, by Starship’s success.

If manufacturing in space sounds too difficult, there’s another manufacturing opportunity—an Alien Dreadnought—and it’s right here on Earth.

Manufacturing and supply chains are currently in pretty much the same state they were 50 years ago, and everyone in the space industry, including SpaceX, Blue Origin, and ULA, partly outsources their manufacturing to many small factories across the US.

While it made sense during the first space race, using mom-and-pop machine shops now is horribly inefficient because 90% of them are too expensive, unreliable, and inconsistent. The archaic supply chain not only increases costs but also lead and iteration times, resulting in launch delays and blown-up rockets.

What we need is an efficient factory that can cover +95% of all space and defense components.

Even though Hadrian is already working on this, the demand for supply chains in the space and defense industries will only continue to grow exponentially, so there’s still room for more manufacturing companies.

When it’s 20x cheaper to launch a satellite, we will see the problem of space junk—the debris that floats in LEO and GEO—intensify to the point when we won’t be able to ignore it any longer. Considering that the worst-case scenario is Kessler syndrome—a catastrophic chain reaction of collisions with the potential to block safe access to space for generations—we will hopefully see the birth of an entirely new sector of “space janitorial services” whose whole purpose will be to clean the debris. Given that there are ~107,000 new satellites planned by 2029, this may become a reality a lot sooner than we think.

Since there are still over 4 billion people without internet access, satellite broadband will continue to grow, representing at least 50% of the global space economy.

If the internetless half of the world isn’t enough to skyrocket the demand for broadband, the rise of self-driving cars, the increasingly ubiquitous IoT devices, and the soaring popularity of video streaming and cloud gaming will undoubtedly help.

Given Starlink’s ambitions to have 42,000 satellites in orbit by 2027 and its current capabilities to build 60 of them per month, I’m not sure if it’s reasonable to enter this market, especially considering that Amazon is launching a constellation of 3,236 satellites for Project Kuiper, and OneWeb is planning to send 48,000 satellites. Even not counting Telesat (1,671 satellites), Viasat (288 satellites), and Mangata Networks (791 satellites), this is the most crowded sector in the Space industry.

Since the majority of these companies are launching their satellites to low Earth orbit, one potential solution is to go higher, to the geostationary orbit (GEO). The caveat here is that GEO satellites are an order of magnitude more expensive to build, at least four times more expensive (per kg) to launch, and have higher latency and lower bandwidth per user than LEO satellites do. On the plus side, since GEO is at ~35,000 km above the Earth’s surface, each satellite gets a much wider field of view, allowing companies to cover most of the planet’s surface with only three satellites spaced at appropriate intervals.

If competing with Starlink in providing internet doesn’t sound too appealing, there are quite a few other, no less exciting, use cases for small satellite constellations.

First, there’s Earth observation (EO) – the most popular one. With a camera as a payload, EO satellites help companies evaluate the progress of a construction site, monitor road traffic, a pipeline, or soil health, track vessels, detect changes in forests, plan urban infrastructure, and much more, thus creating lots of exciting opportunities.

The EO satellite market is an incredibly broad topic, deserving a separate post, so here I’ll focus on two main types of companies and low-hanging fruit.

There are satellite operators and data providers, with publicly traded US giants like Planet, which operates 200+ satellites in orbit, capturing 1.2M high-resolution images per day, Maxar, with 285+ launches and 80+ satellites on orbit, and Airbus, with 70+ satellites across the pond.

While having millions of images and giant datasets is great, not only the current process for purchasing satellite imagery is ridiculously archaic, tedious, and time-consuming, but companies and governments don’t care about the imagery per se; they need actionable data and insights.

That’s where the smaller companies like SkyWatch, Boeing’s subsidiary UP42, Bird.i, RS Metrics, and others come in, and where I think the lowest barrier to entry into the space industry is.

Most of these companies curate satellite imagery from multiple providers, use machine learning to process it, and sell it as a service. One of the RS Metrics products, for example, is a dataset containing traffic data from 65,000 retail parking lots, which can be used to monitor economic growth, value the property, or help retailers manage supply chains.

SkyWatch and UP42 are building APIs for sourcing and processing satellite images, making it easier to build geospatial products. Think Twillio, but for satellite imagery.

The problem is end users don’t care about satellite imagery per se; they need actionable data. So by using these APIs, there’s an opportunity to build a data-processing product for currently underserved industries – maritime, agriculture, and transportation.

Asteroid mining is another exciting and potentially incredibly lucrative market.

Back in 2017, Goldman Sachs predicted that the world’s first trillionaire would make their fortune by mining in outer space.

Asterank estimates that more than 500 of the ~6,000 asteroids in NASA’s database are worth $100+ trillion each. The estimated profit on just the top 10 “most cost-effective” asteroids—the easiest to reach and to mine—subtracting rocket fuel and other operating costs, is around $1.5 trillion.

And, of course, there’s 16 Psyche, with $10 quintillion worth of materials.

What can we get from these asteroids?

Valuable metals and minerals at much higher concentrations than found on our planet: platinum, iron ore, nickel, niobium, yttrium, dysprosium, etc. Platinum is the most interesting and highly disruptive from an economic standpoint. According to now-defunct Planetary Resources, a single asteroid the size of a football field could contain $25B-$50B worth of platinum, or ~10X the annual global mine production. This means that a single successfully mined asteroid would likely crater the global price of platinum.

There’s another compound found in asteroids that’s more interesting from a technological standpoint — water.

Water is easily converted into rocket fuel by splitting the hydrogen from the oxygen in H2O and can even be used unaltered as a propellant. Ultimately being able to stockpile the fuel in LEO would be a game changer for how we access space.

On a sad note, while asteroid mining is a very exciting industry, there’s still not a single company that had any success in any way. The two companies that used to go all-in on asteroid mining—Planetary Resources and Deep Space Industries—are now both defunct – the former have failed to raise additional funding (raised ~$49M during their nine years of existence), the later pivoted towards smallsats, and both were acquired.

Trans Astronautica Corporation and the UK’s Asteroid Mining Corporation still exist, but we have yet to see any meaningful results from them.

We do have three successful asteroid-sampling government missions, though.

First, there was a proof-of-technology Hayabusa (2003-2010) by the Japanese Aerospace Exploration Agency (JAXA), which returned to Earth a sample of material from a small near-Earth asteroid Itokawa.

Then, the Hayabusa2 (2014-2020) repeated its predecessor’s success by returning the sample from asteroid Ryugu (which cost ~$150M).

And finally, NASA’s OSIRIS-REx collected a whooping ~60 grams of soil from asteroid Bennu and is currently on its way back to Earth (expected to return in 2023).

NASA’s bigger Asteroid Redirect Mission—to capture a piece of an asteroid and bring it to orbit around the Moon—was cancMoon by the Trump administration.

While the psychological barrier to mining asteroids is high, the actual financial and technological barriers are far lower, and cheap launch costs could potentially be the infliction point.

I believe that with China’s plans for a Moon base and NASA’s return to the Moon, the firMoonuccessful space mining companies will be the ones extracting water, aluminum, and silicon from, you guessed it, the Moon (with MoMoonxpress (raised $65.5M) and ispace (raised $195.5M), potentially, leading the way), even though, at this point, the potential commercial customers for these upcoming use cases are non-existent.

If you want to dig deeper (no pun intended) into the economic feasibility of asteroid mining, here’s an interesting paper that focuses on supplying water in space and returning platinum to earth.

If we come back to Earth, there’s one sub-industry that stands out and has been one of the few sources of revenue for government programs and private companies alike, and it’s space tourism.

The first space tourist was Dennis Tito, who spent a week on board the ISS in 2001 and reportedly paid $20M for a ride on a Russian Soyuz. Space Adventures arranged this and six more flights since then – a company set up to get private individuals into space.

However, the infliction point for space tourism is happening right now, 20 years later, with the successful fully-crewed flights by Richard Branson’s Virgin Galactic and Jeff Bezos’ Blue Origin.

While we don’t know yet how much Blue Origin rides will cost, Virgin Galactic used to sell tickets for $250K each before getting a backlog of 600 reservations and ultimately suspending sales in 2014, and now has reopened sales at $450K per seat.

Besides fun few-minute rides to the Karman line on New Shepherd (or 20km below that if you’d chosen Virgin Galactic’s SpaceShipTwo), SpaceX plans to use their Starship to fly up to 100 people around the world in minutes, which could revolutionize long-distance travel. From New York to Shanghai in 39 minutes, instead of the 15 hours, it currently takes by airplane? Yes, please.

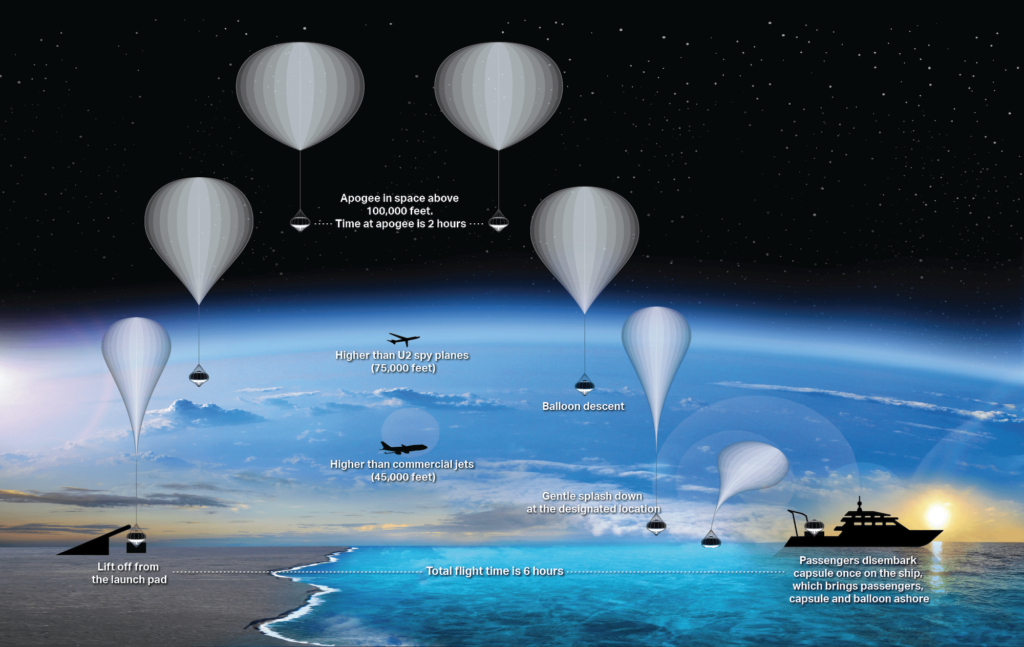

But space tourism doesn’t end with rockets and space planes. There are also space balloons.

Space Perspective offers 6-hour flights to a 30km altitude on a massive 510,000 m^3 space balloon for $125,000 per person. The most interesting part? They already have over 400 seats reserved, and all flights for 2024 are sold out even though they just started accepting reservations earlier this year. While I’m not sure why it’s called a space flight if it only gets you to 30km and you don’t experience weightlessness, it is still a unique experience with a great view. And the demand is clearly there.

Just like tourism on Earth cannot exist with only airplanes and needs hotels, space tourists will also have to stay somewhere once we move beyond fun few-minute rides and ISS gets discontinued.

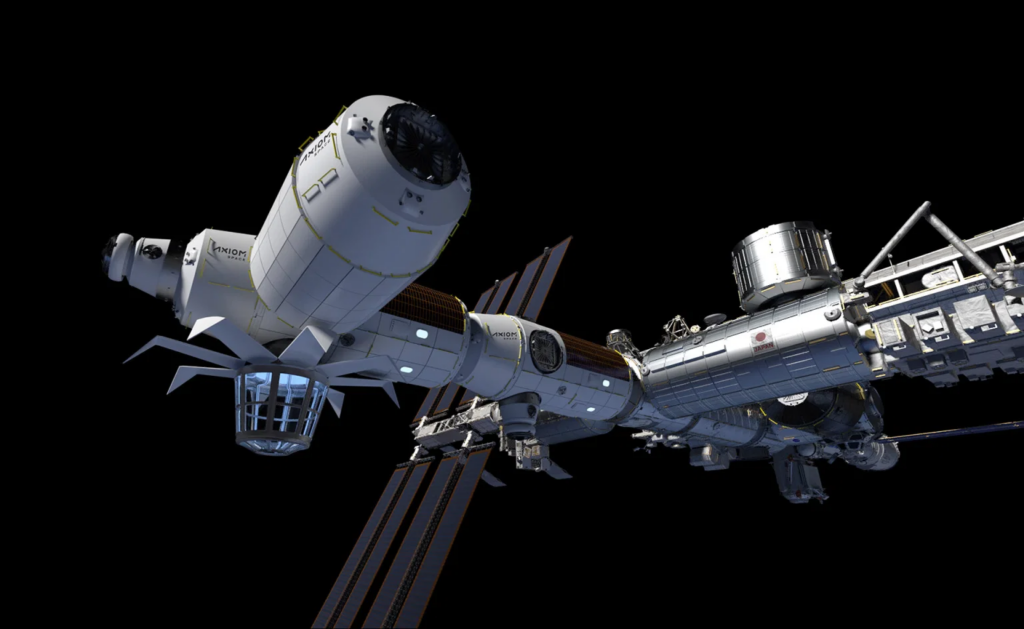

That’s where commercial space stations, aka extraterrestrial hotels, come into play, with Axiom Space currently leading the way.

They plan to start by attaching the first part of its space station to the ISS in late 2024, then add more pieces until it has enough to stand alone, and finally, detach itself and fly as an independent, Axiom-owned space station. Axiom says that they already have more than 20 countries signed up that want a human space program but couldn’t previously afford it.

The first guests to such stations might put up with strenuous ways of conserving water that the astronauts on the ISS endure, but if one enterprising space station offers showers and a good toilet, they’ll be able to charge a premium. That, in turn, will produce a demand for a lot more water, where asteroid and moon mining might come in handy.

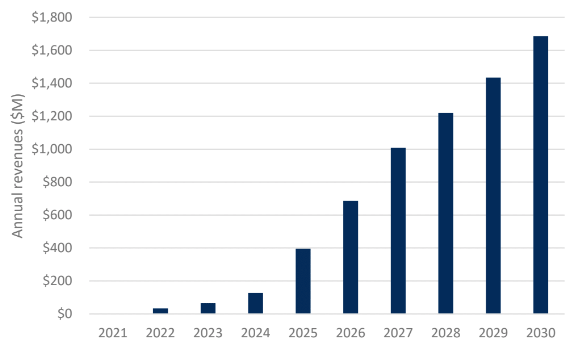

Although today’s space tourism market represents less than $1B of the overall ~$400B space industry, with the addressable market of well over 1 million people that are worth $5M+, there’s general consensus that space tourism will grow at least three to eight times by 2030.

There also could be unexpected and subtler benefits of space tourism. More people will experience the “overview effect,” in which seeing our planet as one borderless, delicate biosphere increases awareness of the fragility and beauty of life. As the vast majority of these space tourists are going to be high-net-worth individuals, perhaps a shift in their perspective will have an outsized influence.

If you noticed, I didn’t mention any opportunities in the launch sector. That’s because I believe it’s already too crowded. There’s only room for ~ ten launch companies for the next couple of decades, and most of the existing launchers will be consolidated.

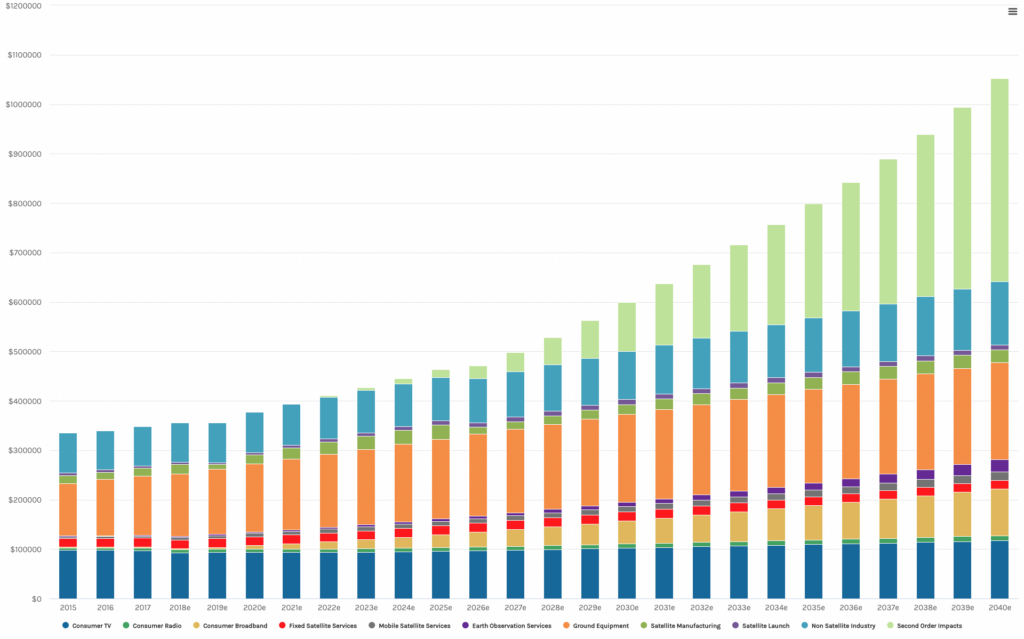

Morgan Stanley estimates that the global space industry will grow to be a $1+ trillion market by 2040, up from the current $350B and $277B in 2010:

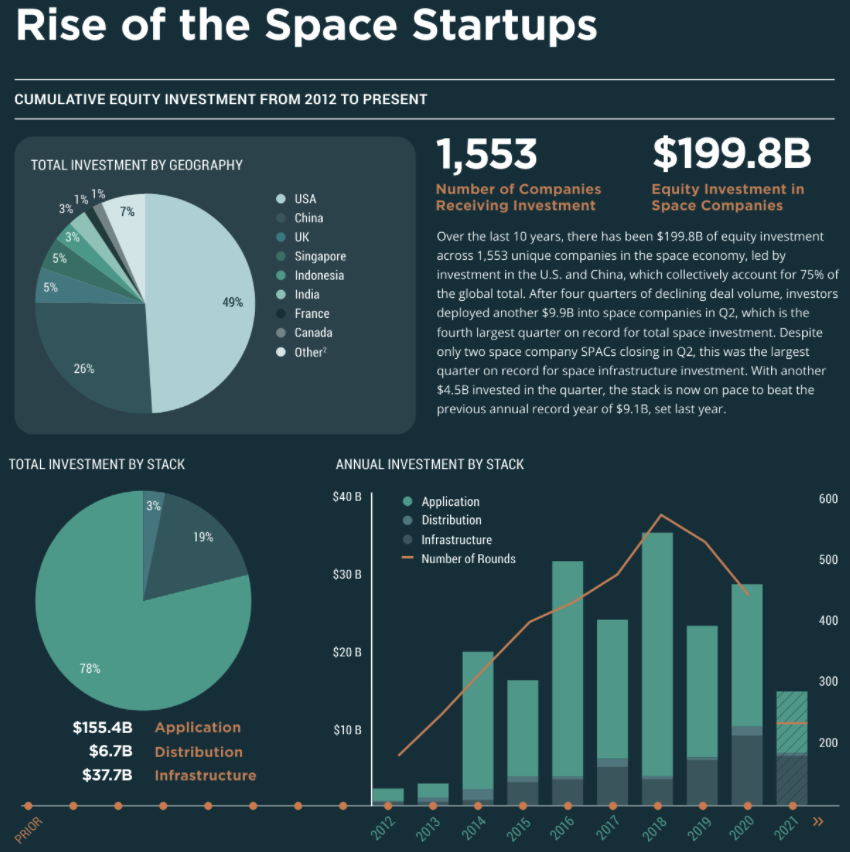

And the investors (Seraphim Space Fund, John Doerr, Khosla Ventures, Sequoia, RRE, Bessemer Venture Partners, Construct Capital, Lux Capital, Founders Fund, First Round, Andreessen Horowitz, Space Capital, among others) are taking notice: Q2 2021 was the largest quarter on record for space infrastructure investment and the fourth largest quarter for total space investment.

I believe that thanks to the advancements of this decade, entirely new markets will be born in space, and 2020s is the best time to enter this industry.

If you’d like to dig deeper into the Space industry, an excellent place to start would be “The Case for Space” by Robert Zubrin and “Space Is Open for Business” by Robert Jacobson.

tl;dr What has changed? Why now?: the space tech advancements of the last decade, the easier access to capital thanks to the success of SpaceX, and, most importantly, the significant drop in the launch costs. If you start now, your product might be ready by the time it costs <$200/kg to get to LEO on a Starship.